Author:Mindao Yang

Mentioned in our previous post — Introduction of dForce’s Multicurrency Asset and Lending Protocol was a Multicurrency Stable Debt protocol built on top of dForce Lending, our upcoming upgrade (expected launch in mid-May) will expand our synthetic protocol beyond over-collateralized stablecoins to other type of assets.

This is the first attempt in DeFi to design a protocol that brings the best out of general lending, native stablecoin and synthetic protocols. It allows to retain the flexibility and asset scalability of a lending protocol, significantly expand the funding source of the synthetic assets, and improve its capital efficiency. We are building a wormhole connecting parallel universes of major crypto assets and synthetic assets.

The lending protocols are divided into two categories. One is a pool-based general lending protocol which supports multisided transactions (supply any supported asset, and borrow others). This is the most general and dominant form of lending protocol in the market; dForce Lending, Aave, and Compound all fall into this category. Second protocol is Maker’s model, which is single-sided, non-pool-based, and unidirectional protocol. They only allow supported collaterals to mint (borrow) DAI, and DAI is the only system debt and users’ debt position are segregated in a siloed position (a.k.a. a CDP).

DAI is a non-pool-based multi-collateral USD synthetic stablecoin. There are several known and long-debated pitfalls of the model:

- Low capital efficiency on the supply side. All collaterals are deposited into siloed CDPs, trading off its opportunity cost (yield) for minting DAI. These collaterals can’t be relent out to generate yield.

- On the output, the only output of the Maker protocol is synthetic DAI (USD-denominated). It is not designed to scale up its offering of other synthetics, i.e., stablecoins in different currencies, such as EUR and JPY or commodity and stocks synthetics.

- Limited output significantly constraint its ability to expand its monetary base and heavily rely on 3rd party support for bootstrapping its liquidity.

From a lending protocol perspective, MakerDAO is significantly less capital efficient and less scalable compared with a general lending protocol. From a synthetic protocol standpoint, the output is also highly constrained by its single synthetic stablecoin design. There are many historical contexts regarding Maker as the earliest DeFi protocol which made many trade-offs along its development and in the process, inherited many technical and design liabilities.

On the synthetic asset side, Synthetix is an important player. It is designed such that its platform SNX is used predominantly as an ingredient for its synthetic assets and though its output synthetic assets are unlimited (unless in absence of oracle price feeds), it has a bottleneck for capacity due to its high collateral ratio (c-ratio) and very limited input (mostly SNX). Synthetix has also long been criticized for its over reliance on SNX as collateral (which could fall into a death spiral when reflexivity unwinds); SNX used to be the only token that can be used to mint synths in their system. Though they lately expanded to include ETH and renBTC as collaterals, non-SNX collaterals only account for less than 1.5% of total system collaterals. This also has many drawbacks:

- Capital inefficiency. With a network c-ratio of 700%, it is extremely capital inefficient;

-

- Supply side constraints. Synthetix is bottlenecked by its input with over 98% its collaterals from their own SNX token, accompanied with high c-ratio; though there is no limit on variety of its synths offering, the capacity of its output is capped by SNX’s marketcap;

- Scalability issue of system debt design. System debt is like a self-financing balance sheet, it is a closed system, which its own stability and expansion highly depending on market reflexivity, it hugely constraints monetary and balance sheet expansion, particularly during a bear market.

So, what we are up to and what are we trying to accomplish?

On a higher level, we aim to design a general lending, native stablecoin and synthetic asset protocol to capture the upsides of three protocols:

- Unlimited input capacity. Basically, all the collaterals supported in the dForce Lending pool (include the supported synthetic assets) are able to be used to mint synthetic assets, there are unlimited supplies and more importantly it bridges between synthetic assets (USX, xBTC …) and other fungible mainstream crypto assets (USDT, USDC, WBTC etc), it runs on an unlimited open balance sheet.

- Unlimited output synthetic capacity. Its offering could include foreign currency denominated stablecoins, USD, EUR, JPY as well as commodities like gold, silver and stocks like TSLA, AAPL and indices like SPX, IXIC. The output capacity is totally independent of DF token’s market capitalization and can be funded by other mainstream crypto assets.

- High capital efficiency. The lending pool collaterals are always yield-on, so using those deposited collaterals to mint stablecoins and synthetic assets, users are compensated for their cost of capital. No collaterals are sitting idle while minting synthetic assets.

- Highly adaptive risk, monetary and fee policies. Different pools could adopt different risk, monetary, and fee policies, i.e., different interest rate for stablecoin and other synthetic assets or different collateral ratio for each asset and each pool, which could accommodate comprehensive variety of use cases.

- Built-in multisided lending support. Synthetic assets are able to be natively supported as lending assets, to be supplied, borrowed and generate yields.

- Building a natively foreign exchange money market. This could foster a truly global interest rate market of different currencies.

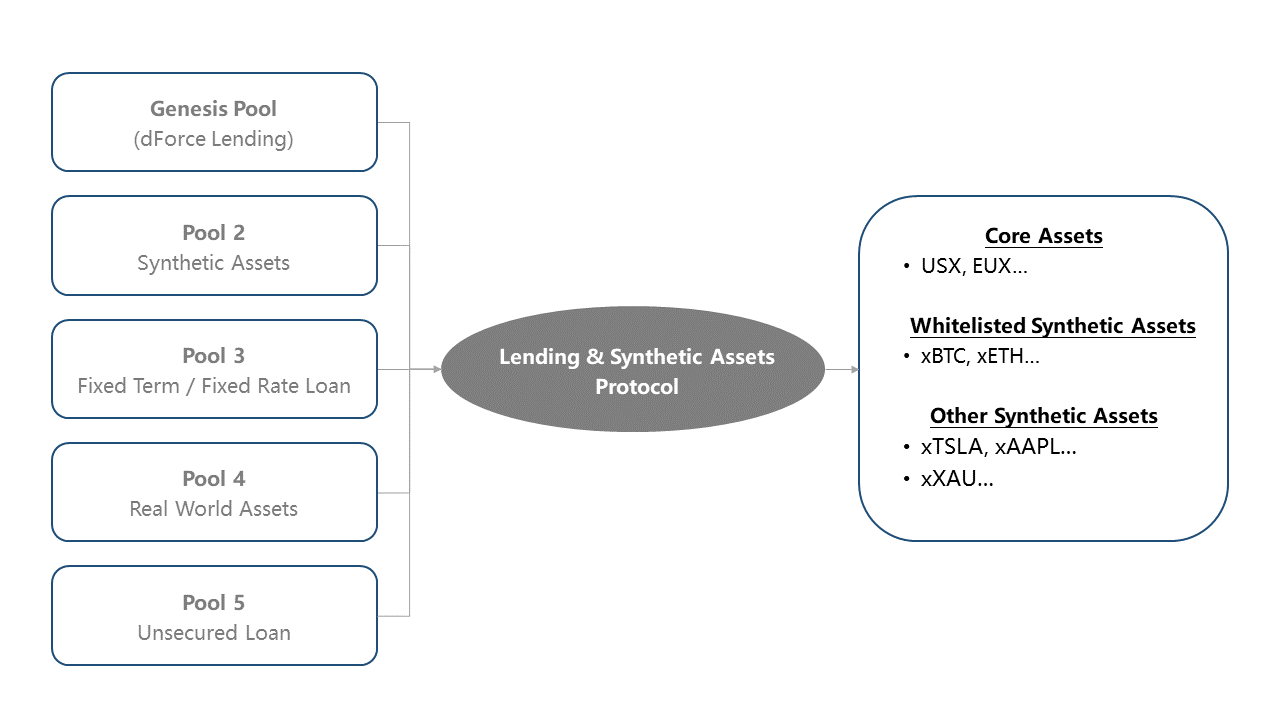

Let’s walk through some of the design specifications on a high level. There will be several pools for the synthetic asset protocol.

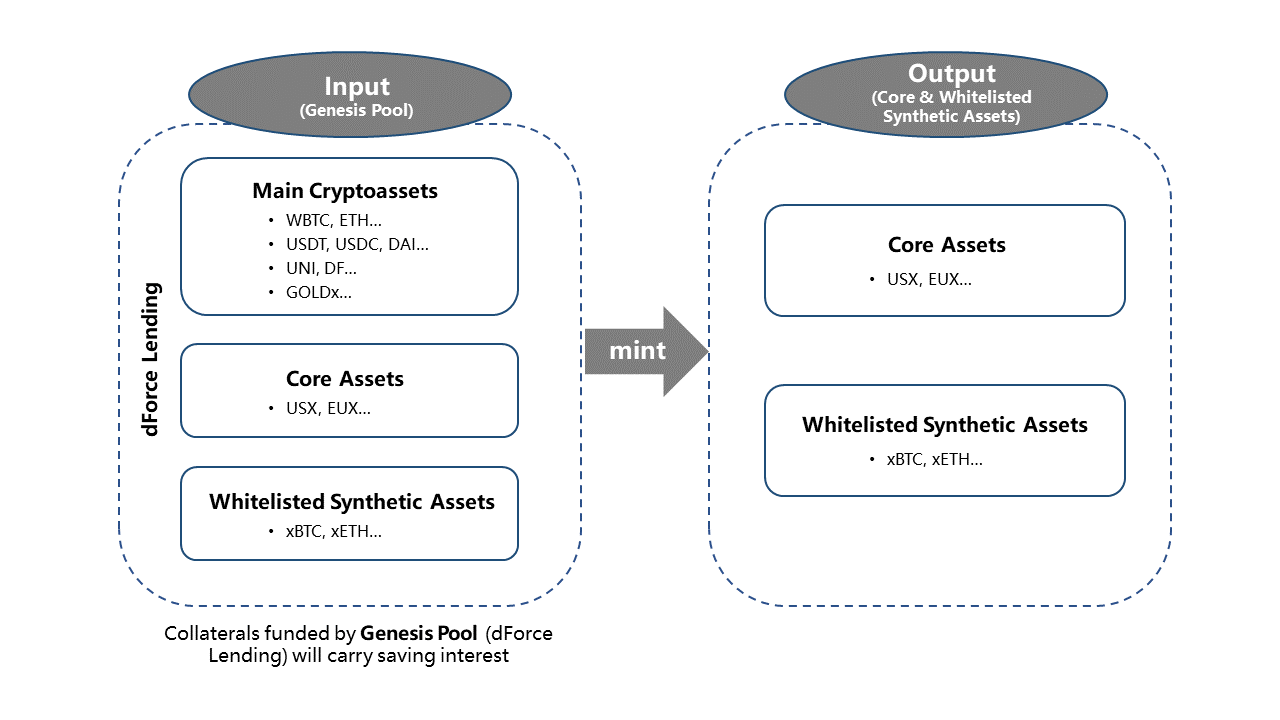

The first pool, the Genesis Pool (dForce Lending Pool), is a pool shared with dForce Lending protocol, where users are able to utilize their supplied collaterals into the lending protocol to mint core assets (over-collateralized stablecoins in different currencies) and other whitelisted synthetic assets

Subject to governance, we propose to have USX, EUX, xBTC, and xETH whitelisted as supported assets to be minted via the Genesis Pool. These assets are also allowed to be supported as collaterals in the lending protocol (subject to governance). So, essentially it is:

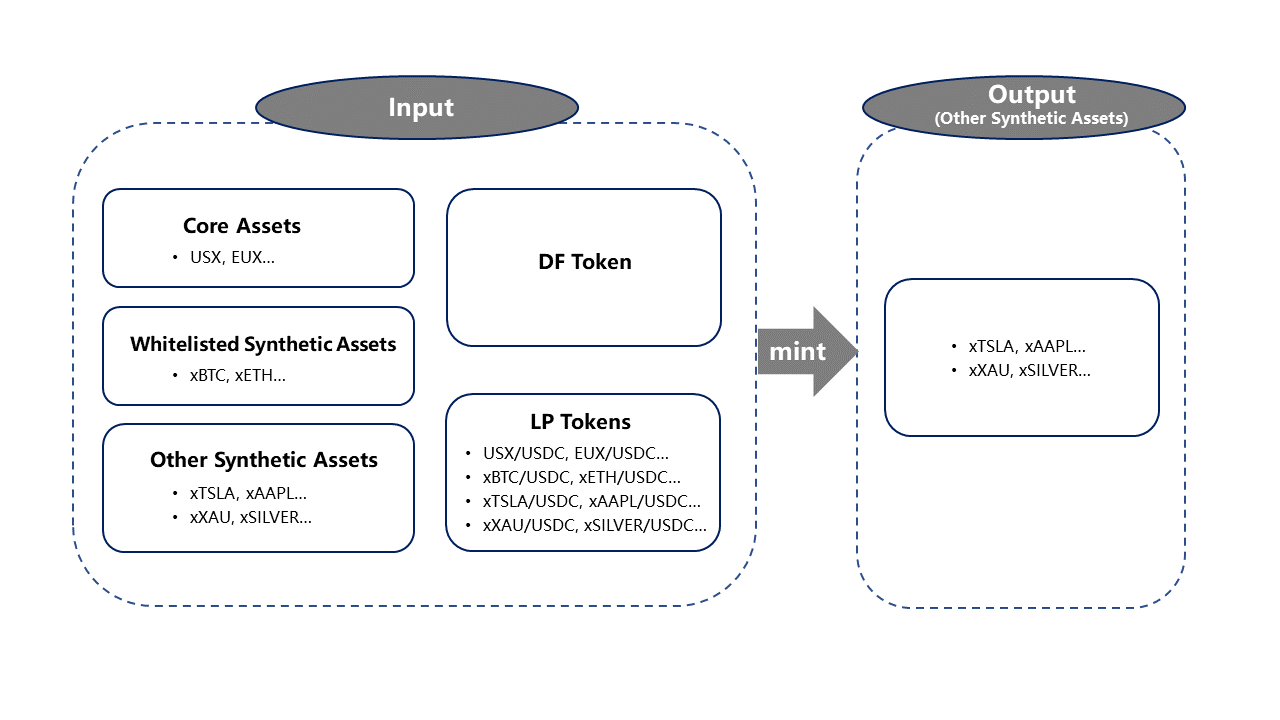

Second pool is the Synthetic Assets Pool . This pool is separated from Genesis Pool (the general dForce’s Lending pool). Collaterals supported in the pool include DF Token, all core assets (USX, EUX) and whitelisted synthetic assets (xBTC, xETH) and potentially other synthetic assets (xXAU, xSilver, xTSLA, xAAPL, etc). In addition to that, to further support liquidity of these assets, a broad variety of synthetic asset LP tokens are also likely be supported as collateral (i.e USX/USDT, USX/EUX, USX/xBTC, USX/ETH, USX/xTSLA, and USX/xAAPL, etc).

Initially, we will disable cross borrowing of synthetic assets in the pool. After the liquidity stabilizes, we could turn on cross borrowing, which allows users to borrow, i.e., xTSLA against collateral of xAAPL. This basically enables margin lending and trading of these synthetic tokens.

In addition to these two pools, other pools could be sprung up to accommodate a broad variety of use cases, i.e.,:

· Facilitate low slippage block trade of crypto assets, such as:

- 10m USDT purchase of ETH or BTC, with combination of liquidity pairs and leverage through our system

- USDT to ETH trade: USX/USDT -> USX/xETH-> xETH/ETH can be accomplished at a slippage comparable to stable asset swap.

· Fixed rate and fixed term loan in synthetic stablecoins, i.e., APY of 3% 3-month USX or EUX loan

· Real world financing (structured loans, real estate financing, etc)

· Unsecured Lending

One of the highlights of the combo is that our synthetic asset protocol natively supports multicurrency stablecoin. Many uses cases can be unlocked; notably:

· Natural Hedge. Borrower to natively hedge their balance sheet risk. It makes little sense for a bitcoin miner in Europe to borrow USD stablecoins, where all their expenses and PPE investments are denominated in EUR. Miners in Europe can borrow EUX using BTC or ETH as collaterals — natively offer FX hedge. This also applies to traders using EUR to denominate their P/L.

· Long/Short Position. Multicurrency support allows traders to capitalize their views on different currencies, i.e., if a trader believes dollar is going to weaken against EUR, they could borrow USX and trade into EUX.

· Low Friction Global Carry Trade. Now, for depositors in Euro zone deep into negative interest rates, it is still very high friction to do carry trade to take advantage of high yield in USD stablecoin yield farming. Traders need to covert EUR into USDC or USDT, which will incur high costs and exposure to FX risk. If we establish a EUX pair, it will be much less friction, when traders with EUR deposit want to participate in the yield farming and other DeFi protocols.

· Global Interest Rate Markets. Given the varying demand and supply, interest rates for USX, EUX, etc will deviate over time and create a vibrant interest rate market globally.

· Global Foreign Exchange Markets. As the demand for different foreign currency denominated stablecoins grow, the liquidity pairs will naturally form and ultimate create a global foreign exchange market supporting multicurrency.

Trading Venues

We will provide the best experience for trading our stablecoin and synthetic assets, trading will be supported in our own dForce Trade portal and we may in the future allow adding liquidity in our AMM; we also embrace other AMMs and DEXs, and will provide incentivized liquidity preferably on AMM with high capital efficiency like Uniswap V3 or Kyber DMM. Given the high gas expenses on Ethereum layer 1, we are also exploring layer 2 and other low gas blockchain like BSC for deploying the upgraded protocols. A more detail liquidity incentive initiative will be announced around the time of the launch.

Interest Rate Policies for Stablecoin and Synthetics

The combo is also going to bring many of the innovations, i.e. in the stablecoin space. We remove Maker’s supply side inefficiency and expand its output to other foreign currency denominated stablecoins. By doing so, we also natively connect other foreign currency denominated stablecoins with unlimited funding assets from the lending protocol.

Similar to DAI and DSR, stable debt in USX and EUX will both have the lending interest rate and supply interest rate, which is native, systematic, and governed by DF tokens holders. However, the Genesis Pool and Synthetic Pool could have different local interest rate policies, though the interest income will still be pooled together across all pools for the same asset.

Aligning with other synthetic protocols, we propose to keep interest rates for other non-stablecoin synthetics at 0% to encourage mintage. Interest rates for stablecoin are also recommended to keep at 0% at initial launch stage.

In addition to native and systematic interest rate policy, dForce Lending can also support USX and EUX as collateral and borrowing assets. Users with these assets can also supply them into dForce Lending to earn interest. Stable debt tokens are just like other stablecoins; their interest rate curve is determined by the liquidity utilization ratio of the asset.

So, the systematic interest rate and lending protocol interest rate can be very different (think the difference between DAI’s Stability Fee/DSR and DAI Borrow/Lending rates on Aave.)

Security

Security is the only thing that keeps the team awake at night. We have engaged 4 top global audit firms for auditing our lending and synthetic asset protocols: Trail of Bits, ConsenSys Diligence, CertiK and Certora (for formal verification) and we also actively engaging with whitehats for bug hunting. All major vulnerabilities were fixed so far. We also implement stringent risk control parameter across assets and 24/7 off-chain monitoring system. Nevertheless, DeFi is uncharted water and there is no guarantee of bug free.

Governance and Value Capture

Now all our important protocol decisions are carried out by DF token voting on snapshot, we want to build our protocol into a minimal governance protocol, with the majority of its parameters (supported collaterals, LTV ratios etc) set by global parameter of the lending and synthetic protocol, which is dictated by DF token holders.

The extension of our lending protocol to native stablecoin and synthetic asset protocol will significantly enhance the value accrual of DF token. Now your DF tokens can be used to mint all synthetic assets in the protocol. Stay tuned for DF Tokenomics 2.0 in the coming weeks!

Acknowledgments: Chao Pan from Maker, Mable Jiang and Multicoin team